How are mortgage rates and inflation related?

Contributed by Karen Idelson, Tom McLean

Updated Dec 16, 2025

•6-minute read

{kind=link}

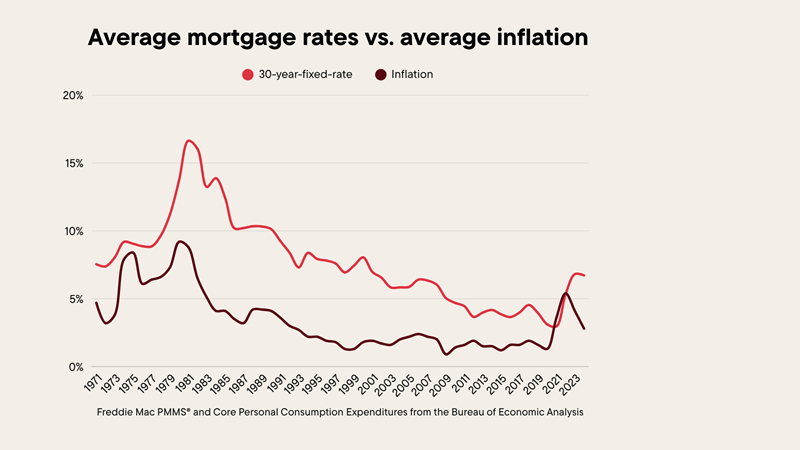

If you’re in the market to buy or refinance a house, you have a stake in making sure that you get the best interest rate possible. So it helps to understand why mortgage rates fluctuate. Part of the reason is inflation, the rate of price increases. We’ll go over the relationship between mortgage rates and inflation.

What is inflation?

Inflation refers to an increase in the prices of the goods and services consumers buy over a period of time. It’s usually measured on a monthly and annual basis. If prices are falling, this is referred to as deflation.

Economists believe that some inflation is a natural part of a healthy economy because it encourages people to buy now before prices rise. This means producers of goods and services can keep people working. What you don’t want is an environment in which prices are rising faster than workers’ wages because this means the relative purchasing power associated with the money they make has gone down in real terms.

There are two primary measures of inflation used in the U.S. – the Consumer Price Index (CPI) from the Bureau of Labor Statistics and the Personal Consumption Expenditures (PCE) Index from the Bureau of Economic Analysis. Although the goal of the metrics is the same, the measurement itself is slightly different based on how spending categories are weighted. For example, housing costs factor more heavily into CPI than PCE.

See what you qualify for

How inflation and mortgage interest rates work together

Mortgage rates are directly tied to mortgage-backed securities (MBS). These are bonds with a return tied to mortgage payments made by homeowners.

If there’s more demand for mortgage bonds, the yield doesn’t have to be as high to attract investors, and mortgage rates are lower. If there’s less demand for MBS, yields and rates are higher to entice buyers. It’s not perfect, but if you’re tracking rates, the closest proxy for MBS demand is the 10-year treasury yield, which runs about 2% below the 30-year-fixed rate.

So what does any of this have to do with inflation? While there’s no direct impact on mortgage rates, inflation tends to correlate with mortgage rates rising. As prices rise, the Federal Reserve raises the federal funds rate to try to get inflation under control. So as prices go up, so will mortgage rates

Although the indexes are different from the 10-year treasury, those with adjustable-rate mortgages (ARMs) will also see the impact of inflation when their rate adjusts, subject to caps. Some of the common indexes used are variations of the Secured Overnight Financing Rate and Constant Maturity Treasury.

In the United States, it’s the job of the Federal Reserve to walk a fine line. As the central bank, officials there have a dual mandate to set the conditions necessary for maximum employment while also maintaining price stability. In doing so, officials have set the long-term goal that inflation should be 2% per year. In September 2025, core PCE – which excludes food and energy and is the Fed’s preferred inflation metric, was 2.8%.

Higher interest rates set by the Fed

The Fed doesn’t exert direct control over mortgage rates or any other consumer interest rate, rather influencing them through the federal funds rate. The federal funds rate is the rate at which federally backed banks borrow from each other overnight to fund their short-term operations. While the actual loan cost is negotiated between the individual banks, the Fed sets a target range that serves as the upper and lower bound for negotiations.

This plays into mortgage rates because the borrowing cost for banks affects the interest that they’ll pay and charge consumers, which has an impact on every other investment market across the country, including treasury bonds and MBS. It may not be a one-to-one movement, but if the federal funds rate moves up or down, mortgage rates often trend in the same direction.

Inflation is still well above the Federal Reserve’s target level, but they’ve been balancing this against concerns over a gradually cooling labor market. As a result, the target range for the federal funds rate has fallen 0.75% in 2025 to 3.5% – 3.75%

While inflation has been edging closer to the Fed’s 2% target, there’s a case that could be made that interest rates could be higher in the coming months. The wildcard for the Fed right now is ongoing tariff imposition and discussion by the Trump White House. The idea is to bring production back to the U.S. by taxing imports, but that takes time. In the interim, tariffs may push prices up. The Fed hasn’t made a move but is eyeing developments.

Higher mortgage rates demanded by investors

A client’s personal mortgage rate is partially influenced by factors like their credit score, down payment or equity amount and how they plan to occupy the home. But that’s after applying a baseline for market expectations. To understand this, it helps to have a basic knowledge of mortgage-backed securities.

When you close on your mortgage, it’s typically sold to a mortgage investor shortly thereafter. These include familiar names like Fannie Mae, Freddie Mac, FHA, and VA. These investors set the qualifying guidelines for the loans they buy so that they can then package loans with similar characteristics into MBS that investors can buy, making money off the principal and interest payments.

MBS can be attractive to investors because mortgage bonds have a certain expected return. They’re more risky than Treasury bonds because these have direct government backing whereas mortgage bonds can fail if there’s too much foreclosure. In practice though, the FHA and VA are government agencies themselves. Fannie Mae and Freddie Mac are government-sponsored enterprises. There’s an implied guarantee of funds.

As mentioned earlier, mortgage rates are tied to the 10-year Treasury, the trading of which is at least somewhat influenced by investors reacting to the moves of the Fed. Further complicating matters, investors are always trying to predict the future because if you close on a mortgage today, it typically doesn’t get packaged into a mortgage bond until a couple months later.

Take the first step toward the right mortgage

Apply online for expert recommendations with real interest rates and payments

What will inflation do to mortgage rates in 2026?

Until time travel becomes a thing, the future is hazy at best. but we can lay out a couple of scenarios that may happen.

First, the case for rates going down. Here, the real key is the labor market. If people start getting laid off in large numbers without finding new jobs quickly, that could lead to a recession. In response to a recession, the Federal Reserve would likely lower the federal funds rate to encourage business investment and consumer spending. Mortgage rates card fall along with interest rates more broadly.

On the other hand, if the labor market holds up and inflation remains elevated, the Fed could hold rates or even push them up in the coming year. Committee members often have differing opinions on the importance of inflation vs. the labor market at any given time. Combine this with less government data than Fed members are used to getting because of the government shutdown and the crystal ball is cloudy at best.

To see how different interest rates affect your monthly payment, check out this mortgage calculator from Rocket Mortgage.

FAQ about mortgage rates and inflation

Those are the basics, but we’ll try to answer a few questions you may still have.

Does inflation affect fixed-rate mortgages?

The impact of inflation on a fixed-rate mortgage is felt when you take it out. However, once you have the mortgage, the rate won’t change, regardless of the level of inflation.

What should I do if I have an adjustable-rate mortgage?

ARMs move up or down with an indexed rate that’s added to a margin after the expiration of an initial fixed-rate period. The movements of these indexes are tied to movements in the bond market, which are influenced by inflation. There are initial, annual and lifetime caps for how much your rate can adjust, but if you think it’ll keep going up, you could choose to refinance to a fixed rate.1

What happens to house prices during inflation?

Home prices aren’t immune to inflation and actually often help drive it. This isn’t all bad. Homeowners like to see the value of their home go up. But if it’s happening, this tends to price potential home buyers out of the market, particularly first-timers who don’t have an existing house to sell while using the money to put toward a new house.

The bottom line: Inflation and the economy may impact mortgage rates

While we’d all love to be able to predict the future, no one can predict interest rates with certainty. The important thing is to make sure you’re comfortable with the monthly payment and that it works with your budget and goals. You can always refinance should rates drop if you maintain good financial discipline. You can begin your mortgage or refinance application online today to take advantage of today’s interest rates.

1 Refinancing may increase finance charges over the life of the loan.

Kevin Graham

Kevin Graham is a Senior Writer for Rocket. He specializes in mortgage qualification, economics and personal finance topics. Kevin has passed the MLO SAFE exam given to mortgage bankers and takes continuing education courses. As someone with cerebral palsy spastic quadriplegia that requires the use of a wheelchair, he also takes on articles around modifying your home for physical challenges and smart home tech. He has a BA in Journalism from Oakland University.

Related resources

8-minute read

How the federal funds rate affects mortgage rates

The federal funds rate helps regulate the U.S. economy, but it can also affect mortgage rates. Learn how it can affect you as a home buyer and homeowner.

Read more

8-minute read

Housing market inflation: What you need to know

Inflation occurs when prices rise relative to the value of the dollar. Learn more about housing market inflation market plus tips for buying.

Read more

8-minute read

How are mortgage rates determined?

Discover what determines interest rates with our in-depth analysis. Explore how economic trends, credit scores, and more impact mortgage rate decisions.

Read more