2026 USDA eligibility map: A guide for home buyers

Contributed by Karen Idelson

Updated Mar 20, 2026

•8-minute read

{kind=link}

If you’re considering buying a home in a rural area but don’t have a lot of funds for a down payment, a USDA loan could be the solution. Backed by the U.S. Department of Agriculture, these loans are designed to help buyers in rural and some suburban areas achieve homeownership, with no down payment required and competitive interest rates. Even if you’re not sure whether a property or community qualifies, the USDA loan eligibility map makes it easy to see which areas are covered.

Rocket Mortgage doesn’t currently offer USDA loans, but we’re here to walk you through how to use the USDA loan map and help you decide if a USDA loan is right for you.

Key takeaways:

- USDA loans expand access to rural homeownership: These loans help low‑ to moderate-income buyers purchase homes in eligible rural and some suburban areas, often with no down payment and competitive interest rates.

- The USDA eligibility map identifies qualifying areas: This online tool highlights eligible zones across the country, with green shading indicating where USDA loans can be used.

- Multiple USDA programs support different needs: Options include single‑family housing direct loans, guaranteed loans, and repair loans or grants, each with its own income limits and qualification requirements.

What are USDA loans?

USDA loans (also called Section 502 loans) are government-backed loans that were created to strengthen rural areas by giving low- to moderate-income individuals and families access to affordable housing options in designated rural areas they might not otherwise qualify for. USDA Section 502 loans offer two main housing programs – direct and guaranteed:

- Single-family housing direct home loans: Here, the USDA acts as your lender, offering very low interest rates to those who qualify based on income limits.

- Single-family housing guaranteed loans: Here, private lenders provide the loan, but the USDA backs it, making it easier for you to get approved with favorable terms.

The USDA also offers Section 504 single-family housing repair loans and grants, providing financial assistance to help existing homeowners repair or improve their rural homes.

Each program has distinctive income limits and requirements, but they all help people build stable lives in rural communities.

“The U.S. Department of Agriculture guarantees these loans, which means participating lenders take on less risk and can offer better terms to borrowers who might not qualify for conventional mortgage loan financing,” says personal finance expert Andrew Lokenauth.

Key USDA loan features

USDA loans offer specific benefits that make homeownership more accessible for qualifying buyers:

- No down payment requirement: Most USDA loans don't require any down payment up front, unless you have substantial assets.

- Fixed interest rates: With a USDA direct loan, you'll get a predictable monthly payment with fixed interest rates as low as 1% to 5%. The lowest rates are reserved for borrowers who qualify for payment assistance based on their income level. USDA guaranteed loans also have fixed rates that vary by the lender and borrower.

- Flexible credit guidelines. “This helps moderate-income families qualify. For example, a teacher in a small town earning a steady income may qualify without a large savings cushion,” Baruch Mann, a personal finance professional, says.

- Extended loan terms: While USDA guaranteed loans have 30-year terms, USDA direct loans offer 33-year terms for most borrowers, with 38-year terms available for very low-income applicants. Home improvement loans through the USDA have 20-year terms.

If you choose a USDA guaranteed loan, you'll pay a guarantee fee of up to 1% of your total loan amount at closing plus an annual fee of 0.35%. The upfront fee helps fund the USDA loan program and can often be rolled into your mortgage, so you don't pay it out of pocket.

Also, keep in mind that if you get a USDA direct loan and later decide to move or sell your home, you'll need to repay any payment assistance to the USDA.

See what you qualify for

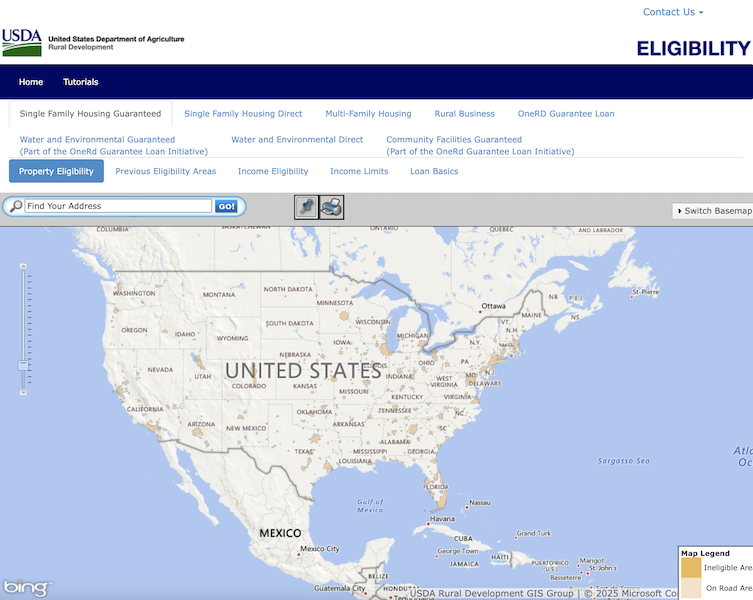

What is the USDA eligibility map?

The USDA eligibility map is a digital tool that shows you which areas across the country qualify for USDA home loans. The map uses population density as its main factor. Areas shaded in white, indicating fewer residents, are more likely to be eligible. Areas shaded in beige usually don’t qualify because they are classified as urban or suburban. Green areas indicate USDA-eligible zones where you can use a USDA loan to purchase a home.

The USDA updates these maps annually, so boundaries can shift as communities grow or change. Make sure to check this map early in your home search so that you don’t fall in love with a property that doesn't qualify for USDA financing. And keep in mind that location eligibility doesn’t necessarily mean you or the property listed meet all criteria necessary for USDA loan eligibility.

Current USDA eligibility map

The interactive map below shows real-time USDA loan eligibility across the U.S. Simply enter an address or zoom in on your area of interest to see whether a property qualifies for USDA financing.

Find the best mortgage option for you

Apply online for expert recommendations and to see what you qualify for

How do you use the USDA loan eligibility map?

To effectively use the USDA eligibility map, follow these steps:

- Visit the official USDA property eligibility website and open the interactive map tool.

- Enter the address of a specific property you're considering or type in a general location like a city or ZIP code to explore the broader area. The map will show you USDA-eligible properties, often in affordable locations and family-friendly areas.

- If a particular address doesn't come up in the search bar, click the pushpin icon located in the toolbar. Click directly on the map location where the house is situated; a pop-up should instantly appear to indicate if that specific coordinate is eligible.

- If you are encountering difficulty identifying exactly where a property sits on the standard map, click the “Switch Basemap” button (in the top right corner). To see actual trees or rooftops, switch to satellite/imagery view, or switch to hybrid view to see street names overlaid atop satellite images.

- Zoom in and out to get a better sense of eligible neighborhoods near your preferred location.

- Ensure that the property falls fully within the approved boundary, even being slightly outside the boundary could make a particular property ineligible.

- Take a screenshot or print the map results for your records and share it with your USDA-participating lender for confirmation. “This step is important because in today’s competitive housing market, you don’t want to waste time making offers on homes that later turn out to be ineligible,” says Mann.

What does property eligibility mean for USDA loans?

When a property is eligible, it means that you can use USDA financing to purchase it. Eligible properties must be located in designated rural areas and meet the USDA's specific requirements for things like size, condition, and intended use.

Depending on the program, you can use USDA loan funds to buy an existing home, build a new one, or renovate a qualifying property.

Be in a rural area

Properties must be located in approved rural areas, which the USDA typically defines as regions with fewer than 35,000 residents. However, don't let the word "rural" fool you. Eligible areas often include small towns and suburbs near larger metropolitan cities.

Area boundaries can be complex and sometimes surprising. Your local USDA Rural Development office can provide the most accurate eligibility guidelines for your specific location.

Serve as your primary residence

The USDA mandates that you must live in the home full-time as your primary residence, as these loans are only for owner-occupied properties. The goal of these loans is to help create affordable housing. You are also required to move in within 60 days of closing and remain in the home for 12 months or more. If you meet the requirements, you may also want to consider a USDA direct loan.

That means investment properties, vacation homes, and rental properties don’t qualify.

“Lenders will verify this carefully, especially in a market where some buyers try to turn homes into income-producing properties,” says Mann.

Thankfully, many property types can serve as a primary residence, including new construction homes, condos, townhomes, manufactured homes, and foreclosed properties.

Be of modest size

USDA loans are intended for modest-sized residences, generally under 2,000 square feet. This requirement exists because these rural housing loans are for buyers looking for reasonably sized family homes, not luxury properties.

But the good news is that there's no limit on the size of the lot your home sits on. You could have a small home on several acres and still qualify for USDA financing.

Be structurally sound and fully functional

Your property must meet basic safety standards to qualify for a USDA loan. This includes having a solid foundation, proper roofing, and fully operational heating, cooling, plumbing, and electrical systems. These requirements protect both you and the USDA.

Pass USDA lender appraisal guidelines

Every property must pass a USDA appraisal before your loan can be approved. This appraisal helps make sure that the home meets all program requirements. The appraiser will:

Verify the home is up to code.

- Establish the home's square footage.

- Establish the number of bedrooms and bathrooms.

- Confirm there are no income-generating structures or prohibited amenities.

Typically, you, as the buyer, will pay for the USDA appraisal, though this can vary depending on your lender's policies.

What are other USDA requirements for borrowers?

These aren't the only rules when it comes to USDA property eligibility. You'll also need to demonstrate your ability to repay the loan and meet the program's income limits. Your household income can't exceed 115% of your area's median income, which varies by location and family size.

“A family of four in one county might qualify at roughly $110,000 in annual income, for example, while the same family in a higher-cost area might qualify at a different threshold,” Lokenauth says.

USDA loans don't have a strict minimum credit score requirement, but having a score of 640 or higher will improve your chances of getting approved and make the underwriting process smoother. That said, if your credit needs work, don’t let that stop you from exploring your options.

When it comes to debt-to-income (DTI) ratio, you also have to stay within certain limits. Your front-end DTI ratio, which is your proposed monthly housing payment divided by your gross monthly income, shouldn’t surpass 29%. Meanwhile, your back-end DTI ratio, which combines your housing payment with all other monthly debts, should not exceed 41% of your gross income (although some exceptions exist).

“You must also demonstrate that you can cover closing costs, even if you finance part of them or negotiate seller credits,” Mann adds.

Check your USDA income eligibility online through the official USDA website to see if you qualify based on your location and household size.

Find out how much you can afford

Your approval amount will give you an idea of the closing costs you’ll pay

What are some alternatives if I’m not eligible?

Can’t find a USDA-eligible property, or don’t meet the borrower requirements? A USDA loan isn’t your only option. Instead, consider these common financing alternatives:

- Conventional loans. These typically require a higher credit score and a down payment of at least 3% to 5%, unlike the zero-down USDA option, and you must pay private mortgage insurance unless you make a 20% or larger down payment. But there are no geographic restrictions as there are for USDA loans.

- VA loans. These are like USDA loans because they require no money down; plus, no mortgage insurance is required. But you must be an eligible veteran, active-duty military member, or surviving spouse, and you must pay a one-time funding fee.

- FHA loans. These can be had for as little as 3.5% down with a 580 or higher credit score1, and they offer lenient credit requirements, which makes them appealing to first-time purchasers. But you must pay insurance premiums that can last for the entirety of the loan unless you later refinance.

- Jumbo mortgages. These are ideal for more expensive residences that exceed the conforming loan limits set by Freddie Mac and Fannie Mae. You’ll need to make a larger down payment (typically 10% to 20%) and have a higher credit score than you would need for a USDA loan.

The bottom line: Check if you qualify for a USDA loan

USDA loans can help you become a homeowner in affordable rural and suburban communities, often with no down payment required. Using the USDA eligibility map early in your search can help you locate areas where this financing option is available, so remember to take advantage of this valuable resource. Just be sure to carefully understand the property and borrower eligibility requirements for USDA loans. If you don’t qualify, you can explore other loan options by reaching out to Rocket Mortgage.

While Rocket Mortgage doesn't currently offer USDA loans, we do offer a guide to USDA loan closing costs to help borrowers understand what they can expect at closing.

1 To qualify for this offer, you must meet all standard FHA eligibility requirements. In addition, your total mortgage payment, including taxes and insurance, cannot exceed 38% of your income, your debt-to-income (DTI) ratio cannot exceed 45%, and you must have 12 months of verifiable housing history immediately prior to your application, no late payments 30 days or greater in the last 12-months, and no derogatory marks on your credit report. Not available on jumbo loans. Asset statements may be needed, no more than 1 day of non-sufficient fund fees are allowed in the most recent 2 months prior to application. Additional restrictions/conditions may apply.

Erik J Martin

Erik J. Martin is a Chicagoland-based freelance writer whose articles have been published by US News & World Report, Bankrate, Forbes Advisor, The Motley Fool, AARP The Magazine, USAA, Chicago Tribune, Reader's Digest, and other publications. He writes regularly about personal finance, loans, insurance, home improvement, technology, health care, and entertainment for a variety of clients. His career as a professional writer, editor and blogger spans over 32 years, during which time he's crafted thousands of stories. Erik also hosts a podcast (Cineversary.com) and publishes several blogs, including martinspiration.com and cineversegroup.com.

Related resources

7-minute read

USDA vs. FHA Loans: Which is better for you?

USDA and FHA loans can offer more lenient requirements for home buyers with low or moderate income. Learn what else these loans can offer and how they differ...

Read more

3-minute read

USDA guarantee fees: What are they and how do they work?

USDA loans may not require a down payment, but they do require guarantee fees. Uncover the meaning and role of a USDA guarantee fee in home buying.

Read more

4-minute read

Do USDA loans require mortgage insurance?

For USDA loans, mortgage insurance isn’t technically required, but there are similar fees. Find out about these attractive mortgage deals for rural hom...

Read more