Earthquake insurance: What does it cover, and do you need it?

Contributed by Tom McLean

Updated Jul 24, 2025

•8-minute read

{kind=link}

Insurance is essential when you own a home. It protects you from paying to repair accidents or unexpected damage out of pocket. However, standard homeowners insurance doesn’t cover damage from earthquakes. For that, you need a separate earthquake insurance policy. Understanding what earthquake insurance covers and your home’s risk of earthquake damage can help you decide if a policy is worth the price.

What is earthquake insurance?

Earthquake insurance reimburses you for financial losses if your home is damaged in an earthquake. Standard renters and homeowners insurance policies don’t cover earthquake damage, so you need to buy a separate policy if your home is at risk.

Policies are available from nonprofit groups such as the California Earthquake Authority or from private insurers. Private insurers may add earthquake insurance as an endorsement on your homeowners policy or create a separate policy for you.

There are two ways earthquake insurance covers losses:

- With traditional earthquake insurance, your insurance company assesses the value of your losses and reimburses you for the amount that exceeds your deductible.

- Parametric earthquake insurance pays a specific, predetermined amount based solely on the size and severity of the earthquake. This allows for quick processing and payouts after an earthquake.

See what you qualify for

Percentage of homeowners with earthquake insurance in each region

Earthquakes occur along tectonic plate boundaries and occur across the United States. The largest earthquake belt is along the West Coast. Eleven percent of the world’s earthquakes and 17.5% of earthquakes in the U.S. occur in Alaska. California, Hawaii, Nevada, and Washington follow in the number of quakes. If you’re selling a home in California, you must disclose if your home is on an earthquake fault line in a natural hazard disclosure report.

The West region has the highest rate of earthquake insurance coverage, according to an Insurance Information Institute poll from 2020, the most recent year available.

| Region | Percentage carrying earthquake insurance |

|---|---|

| Northeast | 21% |

| Midwest | 16% |

| South | 25% |

| West | 28% |

What does earthquake insurance cover?

Earthquake insurance includes:

- Dwelling coverage. Dwelling coverage helps repair or rebuild your home after an earthquake. It may include structures attached to your home, such as a garage.

- Other structures coverage. Earthquake insurance may help pay for repairs to damaged structures on your property that are not attached to your home, such as a barn or shed.

- Personal property protection. Earthquake insurance can cover damage to your belongings, such as furniture and appliances.

- Loss of use. If you can’t live in your home while repairs are being made, your policy may cover additional living expenses such as a rental home or hotel, plus the cost of food.

- Building code upgrade expenses. If you have an older home that is damaged and needs repairs or to be rebuilt, you may need to upgrade the house to meet building codes that have taken effect since it was originally built. This coverage helps cover the costs of these upgrades.

- Emergency repairs. Emergency repairs cover damage that needs immediate attention to protect your home or personal property from additional damage. For example, repairing broken windows.

Take the first step toward the right mortgage

Apply online for expert recommendations with real interest rates and payments

What does earthquake insurance not cover?

Common earthquake insurance coverage exclusions include fire and floods. Earthquake insurance also doesn’t cover damage from nonseismic land movements, such as sinkholes and landslides.

Earthquake insurance also typically doesn’t cover:

- Water supply systems

- Patio covers

- Landscaping

- Aircraft

- Stored data

- Fences

- Watercraft

- Motor vehicles

- Swimming pools and hot tubs

Review your policy to ensure you have proper coverage in the event of an earthquake. For example, check your auto insurance policy to determine how your vehicle is covered in the event of an earthquake. Also, make sure you know how to file a homeowners insurance claim after a natural disaster.

Find out how much you can afford

Your approval amount will give you an idea of the closing costs you’ll pay

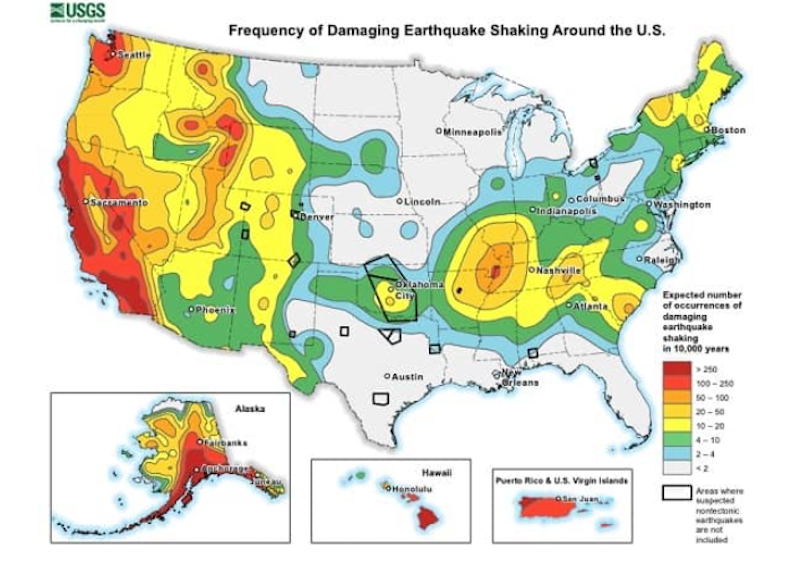

Do I need earthquake insurance?

The first step is to find out your earthquake risk. The U.S. Geological Survey has a map that shows which parts of the country require earthquake insurance.

Source: United States Geological Survey (USGS)

If you don’t have insurance and an earthquake damages your home, you may receive assistance from the Federal Emergency Management Agency. The maximum FEMA payout is $43,600 for housing or other needs assistance, which would not be enough to cover the costs of replacing most homes.

Knowing that, ask yourself this: Would you be able to afford to repair or replace your home after an earthquake without insurance? If you’d need to get a loan, use emergency savings, or access critical resources to fix your home, earthquake insurance may be a good idea.

Learn more about how to recover after a natural disaster.

Determining how much earthquake insurance coverage you need

If you decide to buy earthquake insurance, buy enough to cover your rebuilding costs and personal belongings.

You can start by asking yourself:

- How old is my home?

- Is my home more susceptible to damage?

- What is the current market value of my home?

- How much would it cost to replace my home?

- Have I done an inventory of my belongings?

- Do I have enough money to replace or repair my house without insurance?

- Am I still paying off a mortgage? Would I be paying off my home and covering repair costs?

If you want to cover the full cost of rebuilding your home, determine the average cost per square foot to build in your area. For example, let’s say your home is 3,000 square feet and construction costs about $200 per square foot in your area. In that case, your rebuilding costs would land around $600,000.

An insurance agent or appraiser can help you determine how much earthquake insurance to purchase. An appraiser can also help determine the value of your belongings.

Earthquake insurance in California

Most California residents live within 30 minutes of an active fault line. The California Earthquake Authority is a nonprofit, privately financed, and tax-exempt organization that offers insurance for homes in high-risk areas.

The CEA’s insurance premium calculator can help you estimate the cost of a policy, which will largely depend on:

- Home age and construction

- Earthquake risk location data

- Soil type

- Foundation type

- Roof, construction, and other building materials

How much is earthquake insurance?

Average earthquake insurance premiums cost $800 – $1,350, but can go much higher depending on your property and its location. Deductibles are usually 10% – 20% of your coverage limit. Costs vary, so shop around to find the right policy and price point.

- Your deductible: In general, choosing a higher deductible or coverage leads to lower insurance premiums. Deductibles for this type of insurance policy tend to range from 2% to 20% of the replacement value of your home. If it costs $200,000 to rebuild, you’d be responsible for the first $4,000 with a 2% deductible.

- Location of the home: If your home is in a high-risk area, you should expect to pay more for earthquake insurance. Homes built on sandy soil rather than clay or rock will likely require higher-cost insurance.

- Age of the home: If you have an older home, you’ll likely pay more for coverage. Insuring homes not up to current building codes or those built with brick or masonry will cost more to insure.

- Number of stories in the home: A home with multiple stories will likely cost more to insure than a single-level home.

- Rebuilding cost: The estimated rebuilding costs have a big effect on your insurance costs. The more your home is worth and the more it will cost to rebuild it, the more you’ll pay for insurance.

The cost of earthquake insurance in California

California accounts for two-thirds of the nation’s earthquake risk. Since California is a hotspot for earthquakes, Golden State residents tend to pay higher premiums for insurance. Homeowners in California pay an average of $739 per year for earthquake insurance. Your exact cost will vary based on the amount of coverage you need, the home’s risk, and other factors.

CEA offers the following earthquake insurance options:

- For homeowners. You can buy standard or choice earthquake policies. The standard policy covers earthquake damage to your home and attached structures. Personal property is covered up to $200,000, and additional living expenses are covered up to $100,000. It also covers building code upgrades and emergency repairs. The choice policy includes the standard coverage, plus additional coverage for breakable possessions.

- Mobile and manufactured homes. You can purchase the same type of policies as homeowners insurance, but you cannot obtain coverage for exterior masonry veneer.

- Condominiums. You can purchase several types of optional coverage, calculated as a percentage of the building property's coverage cost. There’s a coverage limit of $100,000 for the condo interior and personal property, with a limit of up to $200,000. You can also get loss assessments from homeowners associations, building code upgrades, emergency repairs, and breakables.

- Renters. Deductibles are calculated as a percentage of the policy limits for personal property, up to a coverage limit of $200,000. Coverage is available for loss of use up to $100,000, as well as emergency repairs and breakables coverage.

How to get earthquake insurance

Getting earthquake insurance is relatively simple.

- Add earthquake insurance to your homeowners policy: You can add earthquake insurance to your existing homeowners insurance policy. Check to see if your insurance company will bundle policies (homeowners, earthquake, auto, etc.), so you can save money with the company.

- Request quotes: Shopping around can help you find the most affordable quote for the type of coverage you need.

- Compare rates: Which company offers the best price? Each insurance company has a slightly different method for determining rates, which can help you shop for a lower price when comparing quotes.

- Choose a policy: Commit to the right insurance quote and company for you, and pay your earthquake insurance premium.

How to save money on earthquake insurance

How can you save money on earthquake insurance? We’ll walk you through knowing your options, gathering quotes, and retrofitting your home.

Know your options

Most insurance companies are private but you can use a government-backed insurance program like the CEA.

Compare quotes

Gather a few quotes to compare, including the different parts of earthquake insurance.

Retrofit your home

Retrofitting your home can save your money on earthquake insurance in California. Retrofitting strengthens your home’s structure against earthquakes and earns you a discount of 10% – 25%. Depending on your income and location, you might be eligible for a CEA grant of up to $3,000 to pay for a seismic retrofit. You also might borrow your home equity with a cash-out refinance or home equity loan to retrofit your home.

FAQ

Here are answers to common questions about earthquake insurance.

Does homeowners insurance cover earthquakes?

No. Standard homeowners insurance policies don’t cover damage caused by earthquakes. You need to buy a separate policy to cover earthquake damage.

How much is earthquake insurance?

California homeowners pay on average $738 per year for earthquake insurance. How much you’ll pay depends on your situation.

How much is the deductible on earthquake insurance?

Deductibles on earthquake insurance policies range from 2.5% – 20% of your coverage limit.

What percentage of people have earthquake insurance?

Only 10% of California residents have earthquake insurance, despite experiencing 90% of the country’s earthquakes. Only 11.3% of Washington’s residents had coverage in 2017 despite having the second-largest seismic market. In the New Madrid fault area in Missouri in 2000, 60% of its residents had coverage, but in 2021, only 11.4% of residents had coverage.

The bottom line: Consider earthquake insurance protection

Insuring your home against earthquake damage requires purchasing a separate policy. Evaluate your location and whether you’d need help paying to repair damage to your home if an earthquake struck. Then, talk to your insurer about adding earthquake insurance and how much it will cost.

Think you might retrofit your home? Explore financing options with Rocket Mortgage®.

Melissa Brock

Melissa Brock is a freelance writer and editor who writes about higher education, trading, investing, personal finance, cryptocurrency, mortgages and insurance. Melissa also writes SEO-driven blog copy for independent educational consultants and runs her website, College Money Tips, to help families navigate the college journey. She spent 12 years in the admission office at her alma mater.

Related resources

6-minute read

Disaster preparedness plan and checklist

A disaster preparedness plan can help keep you and your home safe. Make your family plan early and sign up for emergency alerts so you can act quickly.

Read more

7-minute read

Natural hazard disclosure report (NHD): What it is and what it covers

A natural hazard disclosure report (NHD) shows whether a property is in a flood, fire, earthquake, or dam inundation zone. Learn how to use it before closing...

Read more

6-minute read

A homeowners guide to hazard insurance

Read more