VA loans gain popularity as buyer's market opens doors for service members, veterans

Contributed by Grace Kang

Jun 3, 2026

•5-minute read

{kind=link}

VA loans are becoming more prevalent, helping make homeownership more attainable for eligible veterans and active-duty service members facing elevated housing costs.

The increase comes as more sellers accept offers with lower down payments amid softer competition and slower home sales. At the same time, affordability challenges continue to push buyers toward loan products that reduce upfront costs and monthly payments. VA loans, which typically require little to no down payment and often carry lower mortgage rates than conventional loans, are becoming an increasingly attractive option in today’s market.

Key takeaways:

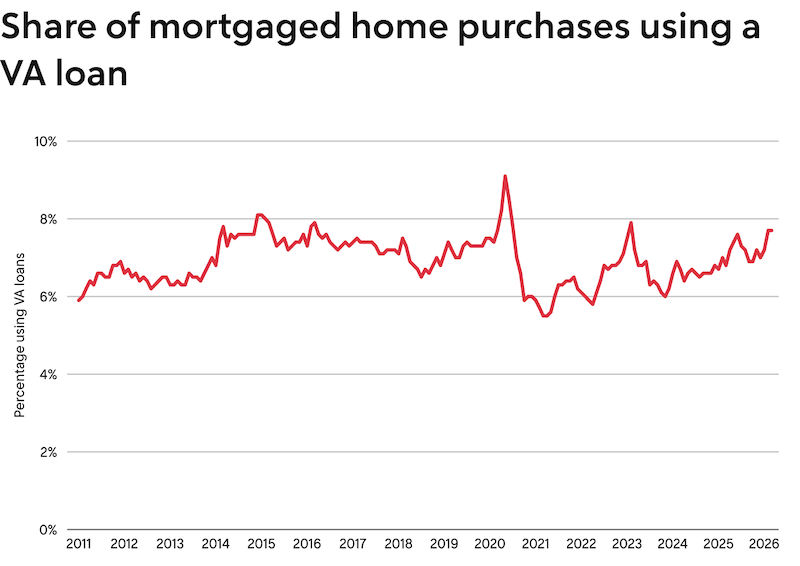

- VA loans accounted for 7.7% of mortgaged home purchases in March, up from 6.8% a year earlier and tied for the highest March share in a decade.

- VA loans were most common in Virginia Beach, Virginia; Jacksonville, Florida; and Washington, D.C.. These are all places with large military presences.

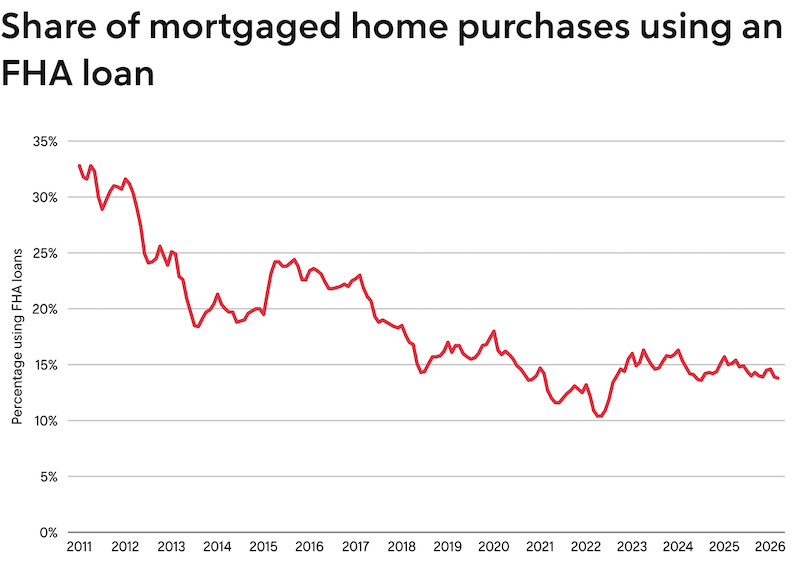

- FHA loans became slightly less common. FHA loans made up 13.8% of mortgaged home purchases in March, down from 15.1% a year earlier.

VA loan usage hits highest March share in 10 years

Nationwide, 7.7% of mortgaged home buyers used a VA loan in March, up from 6.8% a year earlier and tied with 2020 for the highest March share in a decade.

The data in this report is from a Rocket Mortgage and Redfin analysis of county records across 40 of the most populous U.S. metropolitan areas. March 2026 is the most recent month for which data is available. Loan type data is limited to home purchases for which buyers took out a mortgage.

A higher share of borrowers are choosing VA loans as market tilts in buyer’s favor

There are several reasons VA loans are becoming more common:

- It’s a buyer’s market nearly everywhere in the country. That means buyers using a VA loan are more likely to get their offer accepted than when it’s a seller’s market. When sellers have fewer buyers to choose from, they’re much more apt to agree to an offer with little to no down payment. For comparison, competitive markets favor buyers with higher down payments because sellers often feel they’re more financially secure, making the deal more likely to close.

- Affordability challenges are factoring into the buyer’s market and VA loans becoming more prevalent. It’s a buyer’s market because there are hundreds of thousands more home sellers than buyers, a gap caused mainly by weak home buying demand over the last few years. Many would-be buyers are sidelined by high monthly housing costs: U.S. home prices are up 2.4% year over year, and mortgage rates are sitting in the mid-6% range, significantly higher than before and during the pandemic. When monthly costs are high, VA loans help make homeownership more feasible by reducing the amount of cash required for down payments and closing costs.

- VA loans can also help reduce monthly costs. Mortgage rates are typically a bit lower for VA loans than conventional loans.

- The visibility of VA loans has increased significantly. Historically, many eligible veterans didn’t use VA loans because they misunderstood eligibility requirements, thought they were only for first-time buyers, or assumed they were too complicated. Now, lenders and real estate agents have improved education around what VA loans are and how to use them. While recent Rocket data shows that only about half of service members are aware VA loans require no down payment, visibility is better than it was in the past.

“VA loans are one of the most powerful tools available today, especially in a market where affordability remains a challenge for many house hunters,” says Bill Banfield, Chief Business Officer at Rocket. “For veterans and military members, the ability to buy a home with little to no down payment and a lower rate can be the difference between continuing to rent and building long-term wealth through homeownership. Seeing more military families use the benefits they are granted through their service is an encouraging trend.”

Why VA loans still make up small slice of mortgage market

Even though the share of buyers using VA loans has increased, it’s still small. That’s partly because they’re only available to a small portion of the population: eligible veterans, service members, and their surviving spouses. Veterans make up roughly 6% of the U.S. adult population, and active-duty service members make up less than 1%.

FHA loan usage ticks down

Unlike VA loans, the prevalence of FHA loans has declined slightly. Just under 1 in 7 (13.8%) mortgaged home sales used an FHA loan in March, down from 15.1% a year earlier.

FHA loans, meant for low-to-moderate-income borrowers and popular with first-time home buyers, have lower financial requirements than conventional loans. Typically, they require a 3.5% down payment.

Still, conventional loans are far and away the most common type of mortgage. Nearly 4 in 5 (78.5%) home loans were conventional in March, essentially unchanged from a year earlier.

Metro-level highlights: VA loans

The data below is from March 2026, the most recent month for which data is available, and covers 40 of the most populous U.S. metros.

- VA loans were most prevalent in Virginia Beach, Virginia (42.8%); Jacksonville, Florida (18.7%); and Washington, D.C. (16.2%). Those metros all have large military presences.

- They were least prevalent in San Francisco and San Jose, California, where VA loans made up less than 1% of mortgaged home sales. Next comes New York, where just 1.7% of loans were backed by the Department of Veterans Affairs.

- The use of VA loans increased most year over year in Baltimore, Virginia Beach, Virginia; and Nashville, Tennessee.

- Their use fell in 8 metros, with the biggest declines in Providence, Rhode Island; Tampa, Florida; and Denver.

|

Metro-level summary: VA loans and FHA loans, March 2026 |

||||

|

U.S. metro area |

Share of mortgaged home sales using VA loan |

Share of mortgaged home sales using VA loan, YoY change (in percentage points) |

Share of mortgaged home sales using FHA loan |

Share of mortgaged home sales using FHA loan, YoY change (in percentage points) |

|

Anaheim, California |

3.2% |

0.8 |

3.8% |

-0.5 |

|

Atlanta |

8.8% |

1.9 |

19.4% |

-0.6 |

|

Baltimore |

12.6% |

4.6 |

16.2% |

-2.2 |

|

Charlotte |

6.6% |

0.8 |

12.4% |

-2.2 |

|

Chicago |

3.2% |

0.1 |

11.5% |

-0.6 |

|

Cincinnati |

5.8% |

-0.6 |

16.2% |

0.2 |

|

Cleveland |

5.7% |

-0.3 |

15.1% |

0.2 |

|

Columbus, Ohio |

6.7% |

0.5 |

12.3% |

-3.9 |

|

Denver |

6.4% |

-0.6 |

11.7% |

-2.2 |

|

Detroit |

4.5% |

1.4 |

17.5% |

-4.3 |

|

Fort Lauderdale, Florida |

5.6% |

1.1 |

19.6% |

0.9 |

|

Jacksonville, Florida |

18.7% |

2.9 |

15.9% |

-3.6 |

|

Las Vegas |

10.3% |

0 |

22.9% |

-0.9 |

|

Los Angeles |

2.8% |

-0.3 |

13.7% |

0.4 |

|

Miami |

2.1% |

0.3 |

15.5% |

-3.9 |

|

Milwaukee, WI |

4.7% |

0.4 |

10.0% |

0.1 |

|

Minneapolis |

4.5% |

-0.1 |

8.7% |

-0.6 |

|

Montgomery County, Pennsylvania |

3.6% |

0.3 |

10.0% |

2.1 |

|

Nashville, Tennessee |

9.9% |

3.3 |

15.0% |

-3.6 |

|

New Brunswick, New Jersey |

2.5% |

0 |

9.6% |

-0.4 |

|

New York |

1.7% |

0.5 |

7.1% |

-0.7 |

|

Newark, New Jersey |

4.2% |

1.2 |

15.2% |

-0.7 |

|

Oakland, California |

2.6% |

0.6 |

8.5% |

1.8 |

|

Orlando, Florida |

7.6% |

1 |

18.4% |

-3.6 |

|

Philadelphia |

3.4% |

0.9 |

18.8% |

3.7 |

|

Phoenix |

8.8% |

1.6 |

17.5% |

-1.1 |

|

Portland, Oregon |

6.1% |

0.9 |

11.1% |

-2.2 |

|

Providence, Rhode Island |

3.5% |

-3.7 |

10.4% |

-6.8 |

|

Riverside, California |

8.9% |

0.5 |

26.1% |

-1 |

|

Sacramento, California |

5.7% |

-0.3 |

11.7% |

-2.9 |

|

San Diego |

15.6% |

0.6 |

7.4% |

-1 |

|

San Francisco |

0.7% |

0.1 |

1.0% |

-0.4 |

|

San Jose, California |

0.8% |

0.2 |

2.1% |

0.3 |

|

Seattle |

4.2% |

1.4 |

5.4% |

-1.6 |

|

Tampa, Florida |

8.9% |

-1.1 |

22.4% |

-2.6 |

|

Virginia Beach, Virginia |

42.8% |

3.5 |

14.7% |

-1.6 |

|

Warren, Michigan |

5.0% |

0.5 |

10.7% |

0.3 |

|

Washington, D.C. |

16.2% |

0.9 |

10.7% |

-2.4 |

|

West Palm Beach, Florida |

3.9% |

0.5 |

12.0% |

-2.6 |

Rocket Mortgage is a trademark of Rocket Mortgage, LLC or its affiliates.

Rocket Mortgage is a VA-approved lender, not endorsed or sponsored by the Dept. of Veterans Affairs or any government agency.

Dana Anderson

Dana Anderson is a principal data journalist at Redfin, where she has been writing about the numbers behind real estate trends since 2018. She writes data-driven reports about the relationship between mortgage rates and home buying demand, how economic events impact the housing market, and much more.

Related resources

8-minute read

VA loans: Benefits, eligibility requirements and more

VA loans are a way for current and former service members to secure home loans with no down payment. Learn more about the benefits and how to qualify.

Read more

8-minute read

What are the advantages of a VA home loan?

Considering a VA loan to buy a house? Explore the advantages and disadvantages of government-backed loans in 2025.

Read more

6-minute read

Are VA loans assumable? Everything to know about VA loan assumption

Are VA loans assumable? They are, but what does that mean, exactly? Learn everything you need to know about VA loan assumption here.

Read more