How much does title insurance cost? Estimates, requirements, and savings tips

Contributed by Sarah Henseler

Updated Nov 11, 2025

•6-minute read

{kind=link}

Buying a home can be incredibly exciting. But it also comes with some financial risks. That’s why it’s important to protect yourself and your finances even after closing. One way to safeguard your interests is to purchase title insurance. This is a valuable policy that protects both the home buyer and the lender from financial loss caused by title defects and disputes. Title insurance is well worth the relatively small cost, especially considering the peace of mind it provides.

That begs several questions: How much is title insurance? What does it cover? Who pays for title insurance? Why do the costs vary by state? And how can you save money when shopping for title insurance? Let’s take a closer look at what’s involved and what you can expect to pay.

Key takeaways:

- Title insurance is a one‑time closing cost: Unlike other types of insurance, title insurance is paid once at closing and protects against past ownership issues, liens or errors in public records.

- Costs vary by location and home price: The price of title insurance depends on factors such as the property’s purchase price, state regulations and local title company rates.

- There are two types of policies: Lender’s title insurance is typically required by the mortgage lender, while owner’s title insurance is optional but provides ongoing protection for the homeowner.

How much is title insurance?

Title insurance comes in two main forms: lender’s title insurance, which is required; and owner’s title insurance, which is optional but strongly recommended.

Fact is, the cost of lender’s title insurance varies by state, but typically ranges from about 0.1% to 1.0% of your home's purchase price.

Owner’s title insurance, on the other hand, is separate and typically averages at least 0.4% of the home’s purchase price, which often equates to a few hundred dollars (depending on the provider and location). Both types of insurance policies are one-time expenses that you pay at closing.

Imagine your home’s purchase price is $300,000. That means your estimated lender’s title insurance fee will be in the range of $300 to $3,000 (0.1% to 1.0%), as well as $1,200 (0.4%) or more for a separate owner’s title insurance policy.See what you qualify for

What does title insurance cover?

After a property is sold, there’s a risk that someone could challenge the property’s title. Title insurance shields the lender and homeowner against potential legal or financial issues with the home’s title that were not discovered during a previous title search. Think of it as a safety net against unexpected claims or defects related to the property’s ownership history.

Exactly what your title insurance protects against will depend on your title company and the specific policy selected. However, the following are typically covered under most title insurance policies:

- Encroachments

- Disputes pertaining to property ownership

- Liens resulting from incomplete contractor payments, unpaid homeowners association dues, or other outstanding debts

- Forged or falsified documents and deeds

- Other fraud-related disputes

“The good news is that title insurance coverage is in place for as long as the policyholder – meaning you and/or the lender – has an interest in the property, and you’ll only pay for this once at closing,” says Dennis Shirshikov, a professor of economics and finance at City University of New York/Queens College.

Take the first step toward the right mortgage

Apply online for expert recommendations with real interest rates and payments

Why is a title search required with a mortgage?

When applying for a mortgage loan, most lenders will require a title search before closing with your escrow company. This search will confirm that the property being purchased has a clear and undisputed ownership history. A property title search involves a title company examining public records of your property to identify potential legal or financial issues with the property.

Some issues the title company looks for include:

- False signatures or fraudulent claims made against the property

- Clerical errors in the courthouse documents

- Claims for unpaid property taxes

- Claims for workers who worked on the property but were never compensated

- Conflicts between former owners over wills

Thankfully, most homeowners will never need to use their title insurance. Nevertheless, it’s smart to have protection in the rare case any issues arise, especially if a problem was missed during the title search.

Case in point: Let’s say you purchase a home that was part of a deceased person’s estate. However, an unknown inheritor disputes that they own the home, which they claim was illegally sold to you. If a title search had been conducted, your title company would have found documented proof of the inheritor before the transaction closed. If they failed to find proof, your title insurance would assist in covering costs to settle the dispute.

“Your mortgage lender’s financial interest in your property is safeguarded by their lender’s title insurance policy until your loan is paid back,” says Shirshikov. “Meanwhile, for as long as you own the property, your owner’s title insurance policy will safeguard your equity and ownership rights.”

What fees are included in title insurance costs?

When you receive a title insurance quote, the included title company fees may be itemized rather than packaged together in one quote.

Title insurance quote fees may include:

- Title search fee

- Wire fee

- Notary fee

- Endorsement fees

- Transfer tax

- Settlement fee

- Closing protection letter

- Overnight mail charge

- Deed preparation fee

- Government recording charges

- Email/electronic document fee

- Document preparation fee

- Tax and other certificates

Contact your escrow officer if you have any questions about title insurance-related closing costs.

Do title insurance costs vary by state?

Title insurance costs vary based on your location and your home's price.

“The value of your home is the main driver that influences title insurance price. But factors like local regulations, the age of your property – as older properties are more likely to have title issues – as well as individual company pricing all play a role in what you will pay,” says Martin Orefice, CEO of Rent To Own Labs.

The title insurance industry is highly regulated at the state level. That means costs and policies will differ depending on your state and where your property is located.

In states like Florida and Texas, title insurance is regulated and fixed by the state government. Consequently, all home buyers in those states will pay the same rate for title insurance, regardless of insurance provider.

However, in states like Arkansas and Illinois, title insurance rates are unregulated. This allows buyers to shop around and compare title company policy costs to find the best fit. For more information on price regulation and current rules specific to your area, visit your state’s department of insurance website.

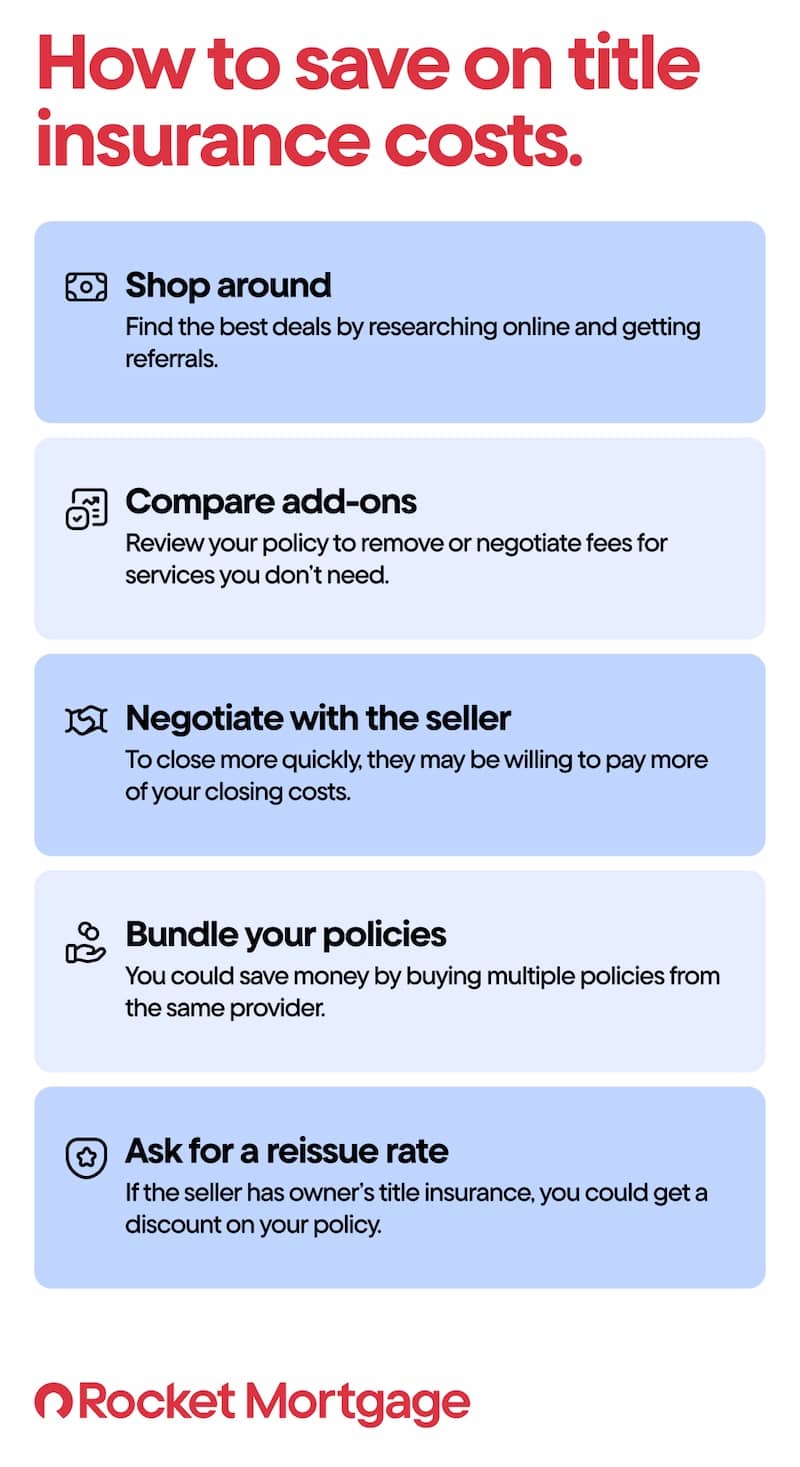

Tips for saving costs when shopping for title insurance

Opportunities exist to save on title insurance, but this will depend on whether your state allows competition among title companies. Here are several proven tips that can help you shave title insurance costs, even in states with highly regulated title insurance companies:

- Shop around: Live in a state with unregulated premiums? Research to find the title company with the best deals. Read reviews and get referrals from friends, family members, and your real estate agent.

- Compare add-ons: Compare and negotiate fees from various title companies. Some companies may include optional services that can be bargained down.

- Negotiate with the seller: Ask your seller to work with you on reducing closing costs. If the seller is eager to close more quickly, they may be open to paying the closing costs themselves. Just be aware that this strategy isn’t recommended if you are in a competitive seller’s market.

- Ask for a bundled policy discount: If you require a lender’s policy but also want added coverage with a separate owner’s policy, learn if you can bundle them together by purchasing from the same provider, which should trim your costs.

- Ask for a lower rate: Does the seller already have owner’s title insurance in place? Ask for a reissue rate, which may yield a discount to you, the next owner.

Note that some savings strategies may not apply in regulated states, but it’s always worth inquiring and understanding what’s negotiable.

For best results, it’s recommended to partner with an experienced real estate agent who knows the most trusted title companies. This expert can point you in the right direction, meaning you’ll spend less time researching and getting preapproved and more time touring potential homes.

FAQ

Here are some commonly asked questions about title insurance costs.

Who usually pays for the lender’s title insurance?

The buyer usually pays for the lender’s title insurance, but owner’s title insurance costs vary by state and can be negotiated. The person responsible for paying the premiums for the owner’s title insurance also varies from state to state. It’s common for sellers and buyers to split title fees into negotiated terms.

How much are title insurance fees?

The cost for a required lender’s title insurance policy is typically 0.1% to 1.0% of the property’s purchase price. The separate expense for an optional owner’s title insurance policy is often 0.4% or higher. Your location, provider, and loan amount will impact your total title insurance fees.

Is title insurance included in your closing costs?

Yes, title insurance costs are usually part of your closing expenses. Before you close, your lender will provide you with a closing disclosure that will detail the expenses due at closing. You should see your title insurance costs included in this section of the document.The bottom line: Title insurance can provide crucial protection when you purchase a home

Buying a home represents a major transaction. It’s important to be legally safeguarded throughout the process, especially with title insurance. This type of insurance protects in the event of title disputes. While most homeowners will never encounter a problem, you’ll want to have protection in place in case an issue arises. Often costing collectively less than 2% of your purchase price for both a lender’s policy and owner’s policy, title insurance can be a small price to pay for peace of mind.

Eager to get the home-buying process underway? Apply for a mortgage online today with the Home Loan Experts at Rocket Mortgage®.

Erik J Martin

Erik J. Martin is a Chicagoland-based freelance writer whose articles have been published by US News & World Report, Bankrate, Forbes Advisor, The Motley Fool, AARP The Magazine, USAA, Chicago Tribune, Reader's Digest, and other publications. He writes regularly about personal finance, loans, insurance, home improvement, technology, health care, and entertainment for a variety of clients. His career as a professional writer, editor and blogger spans over 32 years, during which time he's crafted thousands of stories. Erik also hosts a podcast (Cineversary.com) and publishes several blogs, including martinspiration.com and cineversegroup.com.

Related resources

5-minute read

What does a title company do?

A title company is a third party that works on behalf of both the lender and the buyer. Learn more about what title companies do in the home buying process.<...

Read more

8-minute read

Property title search: How does it work?

A title search examines public records to confirm a property’s rightful, legal owner. Learn how title searches work and what issues they can uncover.

Read more

8-minute read

House title: What you need to know

A house title indicates who has legal ownership of a property and the rights to use it any way they see fit. Learn more about how a house title works.

Read more