Understanding fully amortized loans

Contributed by Sarah Henseler, Tom McLean

Updated Nov 20, 2025

•4-minute read

{kind=link}

A fully amortized loan, also known as a self-amortizing loan, is one with the principal and interest repaid through regular payments over the loan’s term. It’s a loan you pay off gradually over time without needing to make a lump-sum payment at the end.

Mortgages use a formula to calculate a borrower’s monthly payment. This formula ensures that the loan is fully repaid by the end of its term, and that the monthly payments are equal in size if it’s a fixed-rate loan. The results from this formula are laid out in an amortization schedule, which shows how each payment is divided between principal and interest.

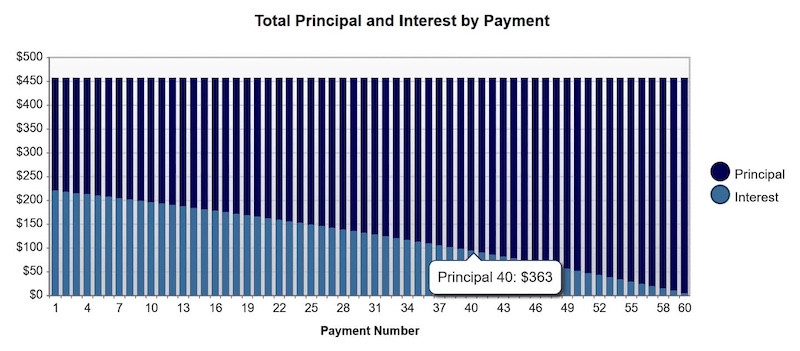

The word amortization simply refers to the process of spreading out loan payments over time, showing how much of each monthly payment goes toward principal vs. interest. At the beginning of the loan term, a larger portion of the payment goes toward interest. As time goes on, the scale tips the other way, and by the end of the loan term, most of the payment goes toward the balance of the loan.

See what you qualify for

How do fully amortizing loans work?

To understand how fully amortizing loans work, it’s helpful to look at one payment at a time.

Much of your first payment goes toward interest, since that’s when the loan balance, on which interest is calculated, is at its highest. A relatively small portion goes toward principal, lowering your outstanding balance.

The second payment works the same way, but because your balance is now lower (thanks to the principal paid in the first payment), the interest charged is slightly less. That allows a slightly larger portion of your fixed payment to go toward principal.

This pattern repeats throughout the loan term: the interest portion of each payment gradually decreases, while the principal portion gradually increases. Over time, the shift accelerates, with principal making up a larger and larger share of each payment.

You can create your own amortization schedule using the mortgage amortization calculator from Rocket Mortgage.

Fully amortizing payments on a fixed-rate mortgage

With a fixed-rate mortgage, your interest rate always stays the same. The only thing that changes is the relative amount of principal and interest being paid month to month. At the start of the loan, you often pay a disproportionate amount in interest. Over time, however, you pay more toward the principal. For example, see the amortization schedule below for a 10-year loan for $100,000 with a 5% interest rate.

Year |

Interest |

Principal |

Ending Balance |

|

1 |

$4,820.42 |

$7,907.44 |

$92,092.56 |

|

2 |

$4,415.86 |

$8,312.00 |

$83,780.56 |

|

3 |

$3,990.60 |

$8,737.26 |

$75,043.30 |

|

4 |

$3,543.59 |

$9,184.27 |

$65,859.02 |

|

5 |

$3,073.70 |

$9,654.16 |

$56,204.87 |

|

6 |

$2,579.78 |

$10,148.08 |

$46,056.78 |

|

7 |

$2,060.58 |

$10,667.28 |

$35,389.50 |

|

8 |

$1,514.82 |

$11,213.04 |

$24,176.47 |

|

9 |

$941.14 |

$11,786.72 |

$12,389.75 |

|

10 |

$338.11 |

$12,389.75 |

$0.00 |

Fully amortizing payments on an Adjustable-Rate Mortgage (ARM)

For adjustable-rate mortgages, amortization follows the same basic pattern: Each payment includes both principal and interest. However, because the interest rate on an ARM changes periodically, the interest charged may increase or decrease over time. As a result, the amortization schedule must be adjusted after each rate change.

For example, if the interest rate goes from 5% to 6%, the interest charged in each payment would increase, and the monthly payment may go up to ensure the loan is still paid off within the original term. However, some ARMs have payment caps that limit how much the monthly payment can increase after a rate change. In such cases, if the new payment isn’t enough to cover the full interest due, the unpaid interest may be added to the loan balance — a situation known as negative amortization.

Take the first step toward the right mortgage

Apply online for expert recommendations with real interest rates and payments

The advantages and disadvantages of fully amortized loans

A fully amortized loan allows you to budget more easily because you know how your monthly loan payment is divided up. Assuming you choose a fixed-rate mortgage, you’ll always know what your mortgage payment will be over the life of the loan. As a homeowner, this predictability is reassuring. It lets you plan ahead by setting aside income to cover your mortgage and using what’s left over on other expenses and discretionary spending.

One drawback of fully amortized loans is that a larger portion of your early payments goes toward interest, particularly within the first few years. This means that if you sell your home early in the loan term, for example, you won’t have much to show in terms of equity. However, the longer you make payments, the more equity you’ll build. Before taking out a fully amortized loan, factor in how long you plan to stay in the home. Selling too soon could limit your financial return.

Find out if a 30-year fixed loan is right for you

See rates, requirements and benefits

How to use an amortization schedule

A home loan uses an amortization schedule to give borrowers a predictable monthly payment and to show how each payment is divided between principal and interest. As a homeowner, you can use the amortization schedule to see your monthly payment, remaining loan balance, and how much you’ve paid in interest.

To pay off your loan early, make extra principal payments, either by regularly adding a bit to each monthly payment or through occasional lump sums. Either way, you’ll reduce the loan balance faster, cutting your total interest costs and shortening the loan term. Just be sure to check that there is no prepayment penalty.

FAQ

Here are answers to common questions about fully amortized loans.

What is an amortization schedule?

An amortization schedule shows how a borrower’s payments are broken down over the life of a loan. Early on, a larger portion of each payment goes toward paying interest. Later, a larger portion of each payment goes toward paying down the principal.

Can I pay off a fully amortized loan early?

Yes. Paying off a fully amortized loan early is a great way to save on interest. But be sure to check that there is no prepayment penalty. If there is, you want to wait until at least the end of that period.

What is a good example of a fully amortized loan?

Fully amortized loans are usually home loans, auto loans, or personal loans. They can be secured with collateral or unsecured.

The bottom line: Amortized loans offer predictability for homeowners

Fully amortized loans offer a clear path to homeownership, with consistent monthly payments and a built-in schedule to pay off your mortgage over time. Whether you’re comparing loan options or planning a repayment strategy, understanding how amortization works can help you make smarter long-term financing decisions.

If you’re interested in a fully amortized home loan, get preapproved for one from Rocket Mortgage.

Christian Allred

Christian Allred is a freelance writer whose work focuses on homeownership and real estate investing. Besides Rocket Mortgage, he’s written for brands like PropStream, CRE Daily, Propmodo, PropertyOnion, AIM Group, Vista Point Advisors, and more.

Related resources

5-minute read

Can you make principal-only payments on your mortgage?

Making principal-only payments on your mortgage can save you on interest over time. Learn how to make a principal-only payment and pay off your loan faster.<...

Read more

8-minute read

ARM vs. fixed-rate mortgage: What’s the difference?

ARMs (adjustable-rate mortgages) and fixed-rate mortgages have distinct pros and cons depending on your goals. Learn the key differences and how to decide.

Read more

12-minute read

What is a 30-year fixed-rate mortgage?

A 30-year fixed mortgage is common among homeowners who prefer stable payments. Learn more about this mortgage so you can decide if it's your best option.

Read more