How are mortgage rates determined?

Contributed by Karen Idelson, Tom McLean

Updated Jun 10, 2025

•8-minute read

{kind=link}

Mortgage rates are based on both market and personal factors. The economy matters. So does your credit score and down payment. Mortgages serving different client bases may have different rates. Lenders set rates based on their operating costs as well. But how are mortgage rates determined? An understanding of this can help you take advantage of opportunities and improve your financial profile to get the best possible rate.

Which economic factors affect mortgage rates?

Many economic and market factors play a big role in general interest rates. Let’s run through some of them.

Financial markets and interest rates

The Federal Reserve is the central bank of the United States. It’s the bank that other banks borrow from when they need to fund their operations. They set the target range for the federal funds rate, which is a range banks negotiate within to borrow funds from each other. When this range goes up, interest rates for all loans tend to rise as lenders pass their increased borrowing costs to the client. The opposite happens when the range falls.

We’ll get into how the Federal Reserve thinks about setting the target range in a minute. For now, you need to know that the market reacts to its decisions. Mortgage rates have less of a reaction because these are longer-term interest rates usually being projected up to 30 years in the future. The yield on the mortgage-backed securities that control interest rates on mortgages are more directly tied to U.S. Treasury yields.

Treasuries and MBSs are both traded in the bond market. Traditionally, the average rate on a 30-year fixed is about 2% higher than the 10-year U.S. Treasury. Beyond that, if you have an adjustable-rate mortgage, these are tied to other market indexes like the Constant Maturity Treasury or Secure Overnight Financing Rate.

See what you qualify for

The overall economy

You may ask yourself why the Fed wouldn’t want low interest rates all the time. If interest rates are too low, people are more likely to spend more money because borrowing is cheap. This means that people are willing to pay higher prices, which can drive inflation up and bring the value of existing savings down. Officials really have to focus on this, so we’ll go into this a bit deeper below. But there are other economic factors to consider.

Spending means people buying, which leads to the production of goods and services, meaning there’s a push and pull between inflation and the labor market. The main goals of the Fed in setting monetary policy are stable prices and the highest possible employment. While the U.S. labor market and inflation rates are its main focuses, the global interconnectedness of the economy means officials have to account for geopolitics.

Inflation

Inflation has specifically been in the Fed’s crosshairs for some time. The Fed began raising interest rates most recently in 2022 after prices had pushed up during and after the pandemic. Of late, officials have begun to push rates down as inflation was getting closer to its 2% annual goal. This level of inflation is seen as enough to keep the economy going by encouraging people to buy now while not deeply eroding existing savings.

The new challenge the Fed is now confronting are the tariffs being put in place by the Trump administration with the idea of tackling the U.S. trade deficit with other countries and the hope of encouraging U.S. manufacturing. The analysis of the Fed and most other economists is that the cost of import taxes is typically passed through to consumers, leading to higher prices.

In combating inflationary pressures, the Fed keeps target interest rates elevated, which decreases Americans’ spending desires and encourages holding onto the money they have. The downside of this is that it means mortgage rates also stay higher.

At the same time, the Fed has to balance inflation against the labor market. If no one is buying, companies decrease production of goods and services. This can lead to layoffs and the potential for a recession, downturn in economic growth. When this happens, the Fed usually lowers interest rates to encourage spending and business investment again.

Essentially, the Fed has to constantly decide whether to apply the brake or the accelerator to the economy. Things are rarely on cruise control.

Lender-specific criteria

Lenders also have their own criteria for setting interest rates based on their operating costs. They may also raise or lower their interest rates depending on their capacity to handle mortgage lead flow at any given time.

If there’s high demand, a lender may have to keep interest rates slightly higher than its competition if it simply doesn’t have enough people in the short term to handle additional volume. But it may lower rates to bring in business when demand is down.

Different mortgage options are also going to present different risk profiles that lenders have to judge. FHA and VA loans may be priced slightly differently than conventional loans, which often have different rates than jumbo loans.

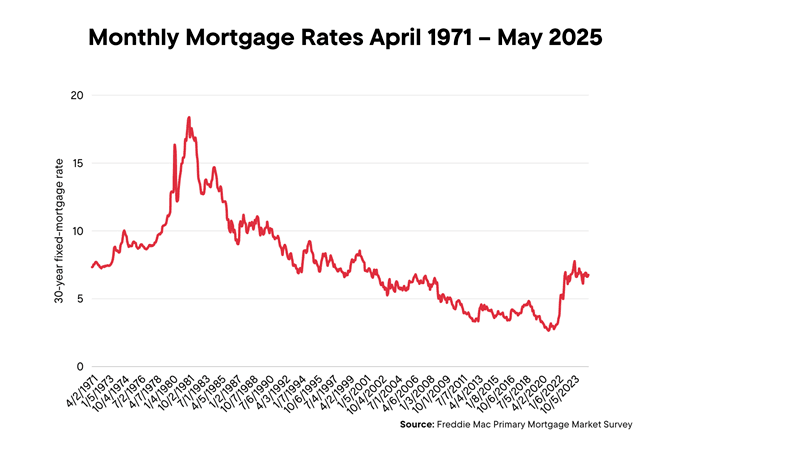

While everything we’ve gone over so far affects market interest rates, if you just want a good idea of where things are at, the Freddie Mac Primary Mortgage Market Survey® has been published weekly since April 1971. Here we’ve shown the data for the first week of each month going back to the beginning of the survey.

What personal factors affect mortgage rates?

While market factors do play a role in mortgage rates, there are also many factors within your personal control.

Credit score

One of the big factors influencing your interest rate is your credit score. Your credit score is a three-digit number that gives lenders a snapshot of how you’ve handled loans and credit in the past. Your score is the median between the three major bureaus, Equifax®, Experian™, and TransUnion®. The standard credit score range is 300 – 850, the higher the better.

If your credit score isn’t where you want it to be, you should first make sure there’s nothing on your credit report that you don’t recognize. You only want to be held responsible for the things you’ve actually done. Doing things like paying down debt and keeping credit card balances to no more than 30% of your overall credit limit will also help you.

You can get your credit report for free once a week from each bureau through AnnualCreditReport.com. This doesn’t show your credit score. Our friends at Rocket Money℠ update your FICO® Score 2 once a month based on Experian™ data.

Down payment

The other primary factor in your interest rate is the size of your down payment. If a lender doesn’t have to give you as much money, the loan is less risky. So the higher your down payment (or equity amount in the case of a refinance), the lower your interest rate will be.

Of course, not everyone can bring 20% down to the closing table, but there may be other resources available. Down payment assistance like grants or deferred, forgivable or traditional loans may be available to first-time or low- to moderate-income home buyers. We recommend looking for programs in your area. Make sure that your lender accepts them. Lenders may reject programs requiring the mortgage to be a secondary lien.

Property type

Your property type also plays a role in the interest rate you get. There are higher rates if it’s a vacation home or rental property than if it’s your primary residence. The idea is that if you ever get into financial trouble, you’re more likely to prioritize the payment on the home you live in most of the time.

There may also be slight adjustments for things like condos. When you live in a condo, you’re responsible for all the maintenance within the four walls of the structure, but if there’s damage to the exterior, that’s usually the responsibility the condo association. A slightly higher interest rate builds in the risk that your condo association can’t keep up its obligations and you can’t repair the home, for example.

Manufactured homes have pricing adjustments, being more susceptible to damage. Finally, properties that have more than one unit see slightly higher rates because homeowners are likely relying on the income from renters to make the payment. If there are long vacancies, this could be an issue.

Debt-to-income ratio

Debt-to-income ratio is the proportion of your monthly pretax income that goes toward debt payments for things like your mortgage, car, student loans, and minimum credit card payments. It’s typically used to qualify you for the loan, but lenders may also sometimes Included in their interest rate calculations. For the purposes of both your interest rate and your ability to qualify, the lower your DTI ratio, the better.

Loan term

The shorter your loan term, the lower your mortgage rate is likely to be. Lenders don’t have to project inflation rates out as far for shorter terms, so you can get a break in the interest rate. On the other hand, while longer terms mean a higher rate, the monthly payment will be lower.

Mortgage points

Mortgage points are prepaid interest paid at closing to buy down your interest rate. When lenders set pricing, specific rates are available based on specific point amounts at given credit scores and down payment amounts. Buying one point costs 1% of the loan amount, but you can buy points in increments down to 0.125%.

The flip side of these are lender credits, which you can think of as negative mortgage points. You might opt for this if you want to keep your closing costs down and have the lender cover these amounts. The trade-off is a higher interest rate over the life of the loan.

Take the first step toward the right mortgage

Apply online for expert recommendations with real interest rates and payments

How can I estimate my mortgage rate?

It can be hard to estimate with exactness what your mortgage rate is going to be because every lender sets rates a little differently. However, they usually have a mortgage rates page. That’s going to show their offered interest rate as well as the annual percentage rate. The APR is the base rate plus closing costs.

They do have to publish the assumptions that advertised rates are based upon. The assumptions are typically things like credit score and loan-to-value ratio – defined as your down payment or equity amount. Based on your qualifications, your rate will be higher or lower, but you can always get a directional sense of how lenders compare with each other and how close you might be to the assumptions.

FAQ

Here are answers to common questions about how mortgage rates are determined.

What determines the interest rate on a mortgage?

Mortgage rates generally are determined by market factors including demand for bonds vs. stocks as well as the federal funds rate. But the other half of the equation is your personal financial picture including your credit score and down payment, as well as the property type you’re looking to buy.

Why do mortgage rates change?

Mortgage rates change based on demand for MBS within the bond market. When people are feeling good about the economy, they tend to invest more in stocks because there is the chance of a higher return. When people don’t feel great about the economy, they tend to invest more in bonds because there’s a guaranteed return.

If more people are flocking to bonds, the yield doesn’t have to be as high and mortgage rates are lower. The opposite tends to be true if more people are optimistic and investing in stocks.

Can I negotiate my mortgage rate?

Your mortgage rate is indeed negotiable. Your lender will have a bottom line, but it doesn’t hurt to ask.

How does my down payment impact my rate?

Because lenders don’t have to loan you as much, they can give you better terms. The higher your down payment, the better.

Are 15-year mortgage rates better than 30?

Mortgage rates for 15-year loans tend to be lower than those for 30-year terms. You’ll find this to be the case with short-term loans in general because the lender isn’t accounting for as many years’ worth of inflation. Even when the actual rate hasn’t changed, you’ll pay less interest with a shorter-term loan.

The bottom line: Mortgage rates are determined by many factors

You can’t control what mortgage rates are going to be, but you can somewhat control getting the lowest interest rate possible at the time by having a high credit score and a sizable down payment. Your loan is less risky in the eyes of lenders. You can also compare interest rates to make sure you’re getting the best possible deal. Just be aware that if you see a much lower interest rate than APR, the lender may be charging higher closing costs to make up for the interest rate.

Ready to buy or refinance and want to look at your real numbers? Get approved online!

Kevin Graham

Kevin Graham is a Senior Writer for Rocket. He specializes in mortgage qualification, economics and personal finance topics. Kevin has passed the MLO SAFE exam given to mortgage bankers and takes continuing education courses. As someone with cerebral palsy spastic quadriplegia that requires the use of a wheelchair, he also takes on articles around modifying your home for physical challenges and smart home tech. He has a BA in Journalism from Oakland University.

Related resources

8-minute read

What are mortgage points and should you buy them?

Mortgage discount points can be purchased to lower the interest rate on a new loan. Use this guide to help you decide if you should buy them.

Read more

8-minute read

How the federal funds rate affects mortgage rates

The federal funds rate helps regulate the U.S. economy, but it can also affect mortgage rates. Learn how it can affect you as a home buyer and homeowner.

Read more

5-minute read

What is APR?

Annual percentage rate (APR) describes the total yearly cost of a mortgage. Learn how to calculate and compare favorable APRs while mortgage shopping.

Read more